Table of Contents

🟢 Section 1: Introduction – Why Personal Finance Tips Matter in 2025

Personal finance tips are more important today than ever before — especially in 2025.

From rising living costs to job market uncertainty and global economic shifts, managing your money wisely is no longer optional. Whether you live in India, the USA, or anywhere else, building a strong financial foundation helps you stay prepared, stress-free, and in control of your future.

But if you’re just starting your journey, it’s easy to feel lost:

- How much should you save?

- Should you invest or repay debt first?

- Is an emergency fund really necessary?

The good news? You don’t need to be a finance expert to manage your money better. You just need the right personal finance tips — practical, beginner-friendly advice that actually works in real life.

In this blog, we’ll break down everything you need to know to get started with personal finance in 2025 — no jargon, no fluff, just clear action steps.

Let’s begin with the basics.

📌 This guide is part of our 🏦 Personal Finance Hub 2025, where you’ll find complete beginner-friendly tips on budgeting, saving, debt, and investing — designed for both Indian and global audiences.

📘 Section 2: What Is Personal Finance? (Explained Simply)

At its core, personal finance tips is all about how you manage your money — how you earn it, save it, spend it, invest it, and protect it.

It’s not just about making more money. It’s about making smarter choices with whatever you have.

🧩 Personal Finance Tips Covers 5 Key Areas:

- 💰 Income Management – Your salary, freelance income, side hustles

- 💸 Budgeting & Saving – How you control your spending and save each month

- 🏦 Investing – Making your money grow through SIPs, FDs, mutual funds, stocks

- 📉 Debt Management – Paying off loans, credit cards, EMIs

- 🛡 Insurance & Protection – Health insurance, life insurance, emergency funds

🤔 Why Is Personal Finance So Important in 2025?

- Inflation is rising across the globe

- Unpredictable job markets (AI, layoffs, gig economy)

- Easy access to debt (credit cards, BNPL) traps people in a cycle

- Most people don’t plan for emergencies — until it’s too late

Whether you’re a student, salaried person, freelancer, or homemaker — understanding personal finance tips helps you:

✅ Reduce stress

✅ Avoid debt traps

✅ Build wealth slowly but steadily

✅ Take better financial decisions for your family

📌 Financial literacy = Life skill. The earlier you start, the stronger your future.

💡 Section 3: 10 Personal Finance Tips for Beginners in 2025

If you’re just starting your financial journey, these personal finance tips are simple, practical, and highly effective — no matter your income level or location.

Let’s break them down one by one:

✅ 1. Track Your Income & Expenses

You can’t manage what you don’t measure.

- Use free apps like Walnut, Goodbudget, or Money Manager to track your spending.

- Know where your money goes — subscriptions, food, travel, etc.

- Build awareness before making any financial decisions.

💡 Small leaks sink big ships — same goes for money.

✅ 2. Set SMART Financial Goals

Define your goals using the SMART method:

Specific, Measurable, Achievable, Relevant, Time-bound.

Examples:

- Save ₹1 lakh for an emergency fund in 12 months

- Start a SIP of ₹2,000/month for 5 years for home down payment

- Clear credit card debt in 6 months

✅ 3. Build an Emergency Fund

- Save at least 3 to 6 months of your monthly expenses in a liquid fund or savings account.

- This protects you from job loss, medical issues, or urgent needs.

- Avoid using credit cards during emergencies.

🚨 Emergency funds are your personal financial “helmet”.

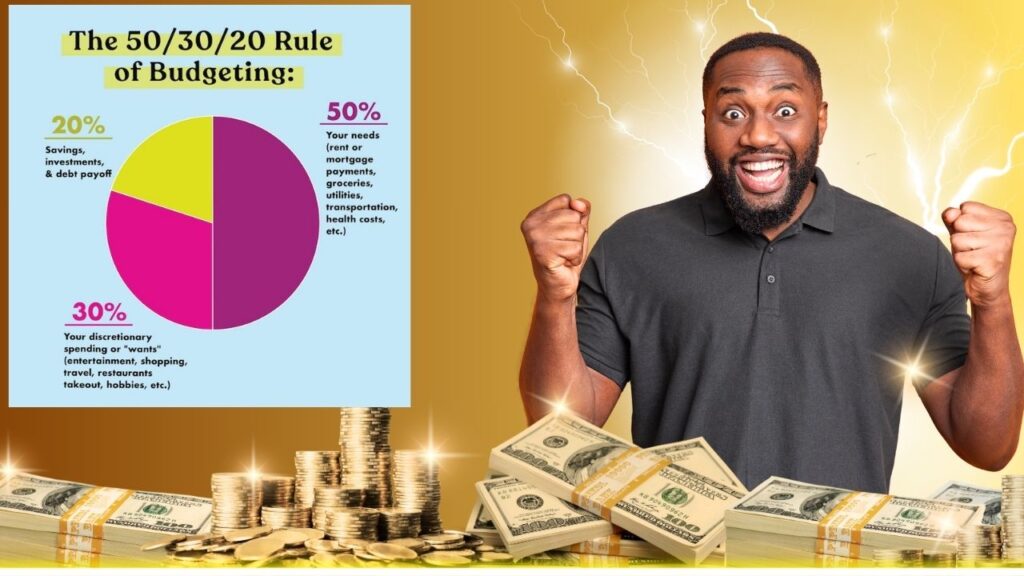

✅ 4. Start Budgeting (Not Just Saving)

Try the 50-30-20 Rule:

- 50% → Needs (rent, food, bills)

- 30% → Wants (entertainment, shopping)

- 20% → Savings & investment

Or go deeper with Zero-based budgeting (assign every ₹/$ a job).

✅ 5. Pay Off High-Interest Debt First

- Focus on clearing credit cards, BNPL (Buy Now, Pay Later), and personal loans.

- Use the Debt Avalanche method: Highest interest first.

Or Debt Snowball: Smallest debt first to build momentum.

✅ 6. Start Investing Early – Even ₹500/Month Matters

- Use SIPs, FDs, or NPS — depending on your goal and risk comfort.

- Investing early = more time for compounding to work in your favor.

- Even small amounts add up over 5–10 years.

⏳ Delay = Missed returns. Start small, stay consistent.

✅ 7. Get Insurance (Term + Health)

- Term Life Insurance (not ULIPs or endowment): Protects your family if anything happens.

- Health Insurance: Avoid draining savings in medical emergencies.

- Don’t depend only on your employer-provided policy.

✅ 8. Use Credit Responsibly

- Keep credit card utilization below 30%

- Pay full bill, not just the minimum due

- Don’t take loans for lifestyle upgrades

💳 Good credit = Better future loan approvals and interest rates

✅ 9. Avoid Lifestyle Inflation

- Don’t increase your spending just because your salary increased

- Save or invest the hike first, then upgrade lifestyle

- Stay grounded even when income grows

✅ 10. Learn Before You Invest

- Read blogs (like StartupJackpot 😉), watch videos, join finance communities

- Avoid “hot tips” and YouTube get-rich-quick schemes

- Understand risk before putting your money in any product

These 10 personal finance tips form the foundation of financial freedom — whether you’re 20, 30, or 50 years old.

🚫 Section 4: Personal Finance Mistakes to Avoid

Even smart people make financial mistakes — often not because they lack money, but because they lack a plan. Avoiding these common traps will save you years of regret and help you stay ahead in 2025 and beyond.

Here are the top mistakes to watch out for:

❌ 1. Not Following a Budget

Living without a budget = financial blindness.

Even a simple monthly plan helps avoid overspending and builds awareness.

📌 No budget? No control.

❌ 2. Living Paycheck to Paycheck

Spending everything you earn (or more) leaves no room for saving, emergencies, or growth.

Start small — even saving ₹500 or $20/month matters.

❌ 3. Delaying Investments

Waiting for the “right time” is a myth.

The earlier you start investing, the more compounding works in your favor.

⏱ Time in the market > Timing the market.

❌ 4. Taking Loans for Wants, Not Needs

Buying a phone, vacation, or iPad on EMI feels tempting — but it locks your future money for temporary pleasure.

Use loans only for assets (education, business, emergencies).

❌ 5. Ignoring Insurance

Medical bills can wipe out years of savings.

Health and term insurance are non-negotiable if you have dependents or unstable income.

❌ 6. Following Trends Without Research

Everyone investing in crypto? A new IPO looks flashy?

Unless it fits your goals, skip the herd mentality.

📉 Trend-based investing leads to regret-based outcomes.

❌ 7. Not Tracking Net Worth

Savings = Good

Investments = Better

Knowing your net worth = Best

Track it yearly — assets minus liabilities — to see your real progress.

❌ 8. Depending Only on a Salary

2025 is uncertain — layoffs, AI, and inflation are real.

Develop multiple income streams: freelancing, content, rent, dividend, etc.

Avoiding these mistakes will save you more money than any investment tip can earn.

🧰 Section 5: Tools & Apps to Manage Personal Finance in 2025

Managing your money doesn’t have to be manual or complicated anymore. Thanks to modern tech, there are dozens of free and user-friendly apps to help you track expenses, set goals, invest smartly, and stay in control — whether you’re in India, the USA, or anywhere globally.

Here are the best personal finance tips tools for 2025:

📱 1. Expense Tracking & Budgeting Apps

| App Name | Region | Features |

|---|---|---|

| Walnut | India | SMS-based expense tracker, bill alerts, budget summaries |

| Goodbudget | Global | Envelope budgeting system, great for beginners |

| Money Manager | Global | Manual entry, offline mode, income-expense analysis |

| YNAB (You Need A Budget) | USA/Global | Advanced zero-based budgeting, syncing, goal planning |

📊 2. Investment Platforms

| Platform | Region | Features |

|---|---|---|

| Groww | India | SIP, stocks, gold, FD, PPF – beginner-friendly UI |

| INDmoney | India/USA | Global investing, credit score tracking, goal planning |

| Zerodha Coin | India | Direct mutual fund investments with no commission |

| Robinhood | USA | Stocks, ETFs, crypto, commission-free trades |

🧮 3. Calculators & Planners

- SIP Calculator – Estimate wealth creation from monthly investments

- FD Interest Calculator – Know your returns post-tax

- Retirement Planner – Figure out how much to save for old age

- Loan EMI Calculator – Avoid loan traps with clear repayment plans

You can find many of these tools directly on StartupJackpot.com/tools (🔧 coming soon).

🧠 4. Learning Platforms for Financial Literacy

- Navi Learn (India)

- Khan Academy – Finance Section

- MyMoney.gov (USA Govt)

- Coursera/Udemy – Personal Finance Tips Courses

📌 Pro Tip: Use one app from each category — don’t overload yourself. Simplicity = consistency.

👥 Section 6: Real-Life Examples (India + USA)

It’s one thing to read personal finance tips — it’s another to see how real people apply them. Let’s explore two beginner-friendly case studies — one from India and one from the USA — to show how small changes can lead to big financial results.

🇮🇳 Case Study: Riya, 28 – Salaried Professional in Kolkata, India

Example Scenario

Inspired by Finance patterns

Typical story based on observed trends

- Income: ₹35,000/month (after tax)

- Challenge: Living paycheck to paycheck, no savings

- Goal: Build emergency fund + start investing + reduce credit card debt

🧭 Riya’s Plan Using Our Personal Finance Tips:

- Budgeted using 50-30-20 rule:

- Needs: ₹17,500

- Wants: ₹10,500

- Savings & Investments: ₹7,000

- Built ₹30,000 emergency fund in 6 months (liquid FD)

- Started ₹2,000/month SIP in a balanced mutual fund

- Closed credit card debt in 5 months using the avalanche method

- Took ₹5 lakh term life insurance and ₹3 lakh health insurance

🟢 In 12 months, she went from financial stress to financial confidence.

🇺🇸 Case Study: Michael, 32 – Freelance Graphic Designer in Texas, USA

Example Scenario

Inspired by Finance patterns

Typical story based on observed trends

- Income: ~$4,500/month (variable)

- Challenge: Irregular income, no retirement plan

- Goal: Track finances better, invest for retirement, control spending

🧭 Michael’s Plan Using Our Personal Finance Tips:

- Used Goodbudget to create envelopes for rent, bills, food, savings

- Set up automatic $200/month into Roth IRA

- Used YNAB to plan for variable months with less income

- Paid off $2,000 credit card debt using snowball method

- Saved $3,000 in emergency fund (high-yield savings account)

🟢 In just 8 months, Michael reduced stress and started building long-term wealth.

🔑 Takeaway: No matter where you are or how much you earn, these personal finance tips are adaptable, actionable, and life-changing.

🏁 Section 7: Final Thoughts + Related Resources + Disclaimer

Managing money doesn’t require a finance degree — it just requires the right personal finance tips and the willingness to act.

Whether you’re in India, the USA, or anywhere in between, the habits you build today can lead to freedom, security, and opportunities tomorrow. Start with small steps: track your spending, save for emergencies, begin a SIP, and stay away from debt traps. The sooner you start, the easier it gets.

🔗 Related Content You’ll Love

- 📘 SIP vs RD vs FD: Which is Better for You in 2025?

- 📘 Top Low-Investment Business Ideas for India & USA in 2025

- 📘 How to Make Passive Income Online in 2025

- 📘 How to Start a SIP with Just ₹100 – Step-by-Step Guide

🛡️ Disclaimer

This blog is for educational purposes only. StartupJackpot.com does not offer personalized financial advice. We are not SEBI-registered or certified investment advisors. Please consult a registered financial planner before making any major investment or insurance decision. Past performance is not a guarantee of future results. Some links may be affiliate links at no extra cost to you.

1 thought on “Personal Finance Tips for Beginners: Build a Strong Money Foundation in 2025”